We will learn more in the coming weeks about the fate of the proposed American Innovation and Choice Online Act (AICOA), legislation sponsored by Sens. Amy Klobuchar (D-Minn.) and Chuck Grassley (R-Iowa) that would, among other things, prohibit “self-preferencing” by large digital platforms like Google, Amazon, Facebook, Apple, and Microsoft. But while the bill has already been subject to significant scrutiny, a crucially important topic has been absent from that debate: the measure’s likely effect on startup acquisitions.

Of course, AICOA doesn’t directly restrict startup acquisitions, but the activities it would restrict most certainly do dramatically affect the incentives that drive many startup acquisitions. If a platform is prohibited from engaging in cross-platform integration of acquired technologies, or if it can’t monetize its purchase by prioritizing its own technology, it may lose the motivation to make a purchase in the first place.

This would be a significant loss. As Dirk Auer, Sam Bowman, and I discuss in a recent article in the Missouri Law Review, acquisitions are arguably the most important component in providing vitality to the overall venture ecosystem:

Startups generally have two methods for achieving liquidity for their shareholders: IPOs or acquisitions. According to the latest data from Orrick and Crunchbase, between 2010 and 2018 there were 21,844 acquisitions of tech startups for a total deal value of $1.193 trillion. By comparison, according to data compiled by Jay R. Ritter, a professor at the University of Florida, there were 331 tech IPOs for a total market capitalization of $649.6 billion over the same period. As venture capitalist Scott Kupor said in his testimony during the FTC’s hearings on “Competition and Consumer Protection in the 21st Century,” “these large players play a significant role as acquirers of venture-backed startup companies, which is an important part of the overall health of the venture ecosystem.”

Moreover, acquisitions by large incumbents are known to provide a crucial channel for liquidity in the venture capital and startup communities: While at one time the source of the “liquidity events” required to yield sufficient returns to fuel venture capital was evenly divided between IPOs and mergers, “[t]oday that math is closer to about 80 percent M&A and about 20 percent IPOs—[with important implications for any] potential actions that [antitrust enforcers] might be considering with respect to the large platform players in this industry.” As investor and serial entrepreneur Leonard Speiser said recently, “if the DOJ starts going after tech companies for making acquisitions, venture investors will be much less likely to invest in new startups, thereby reducing competition in a far more harmful way.” (emphasis added)

Going after self-preferencing may have exactly the same harmful effect on venture investors and competition.

It’s unclear exactly how the legislation would be applied in any given context (indeed, this uncertainty is one of the most significant problems with the bill, as the ABA Antitrust Section has argued at length). But AICOA is designed, at least in part, to keep large online platforms in their own lanes—to keep them from “leveraging their dominance” to compete against more politically favored competitors in ancillary markets. Indeed, while covered platforms potentially could defend against application of the law by demonstrating that self-preferencing is necessary to “maintain or substantially enhance the core functionality” of the service, no such defense exists for non-core (whatever that means…) functionality, the enhancement of which through self-preferencing is strictly off limits under AICOA.

As I have written (and so have many, many, many, many others), this is terrible policy on its face. But it is also likely to have significant, adverse, indirect consequences for startup acquisitions, given the enormous number of such acquisitions that are outside the covered platforms’ “core functionality.”

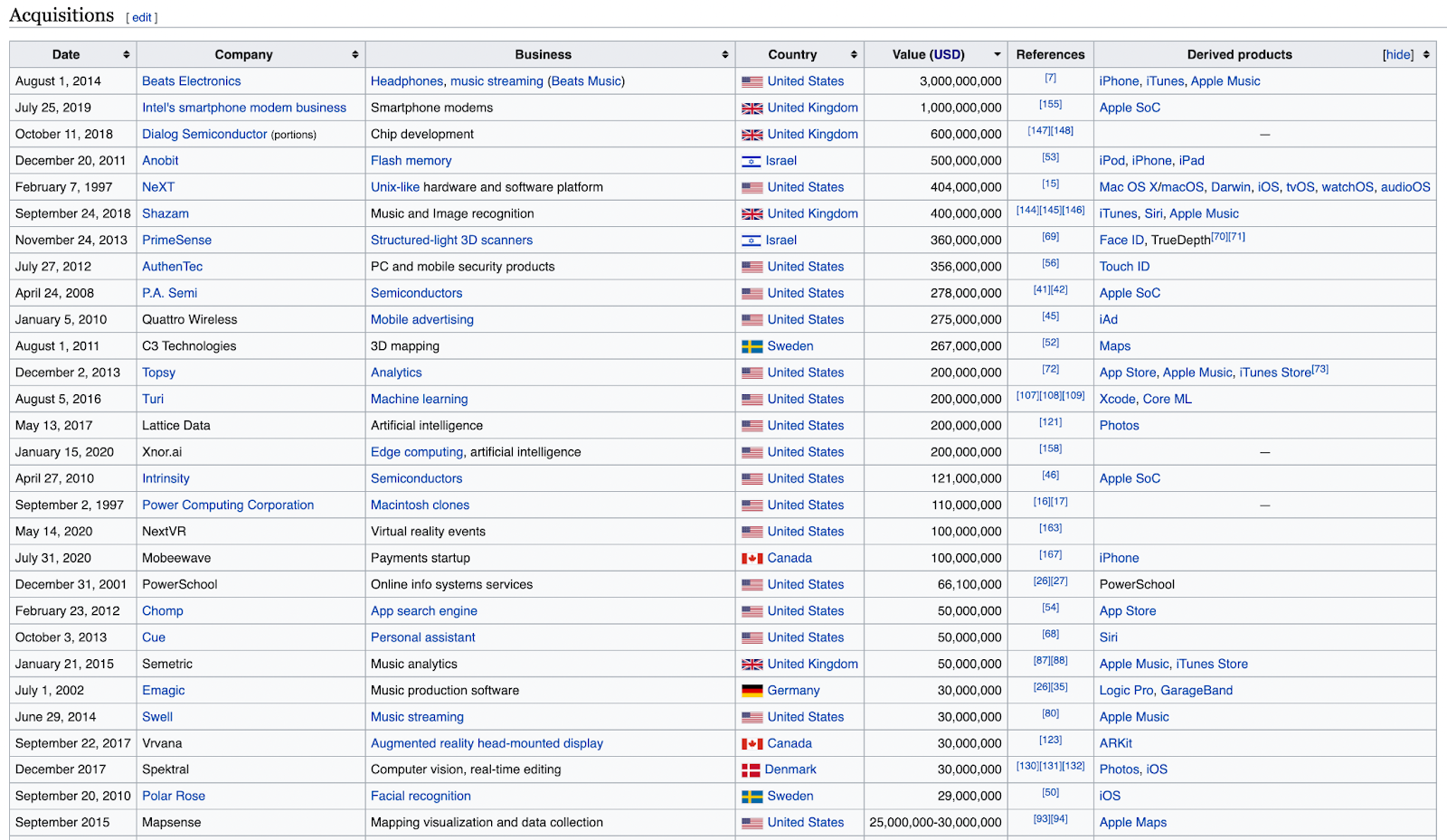

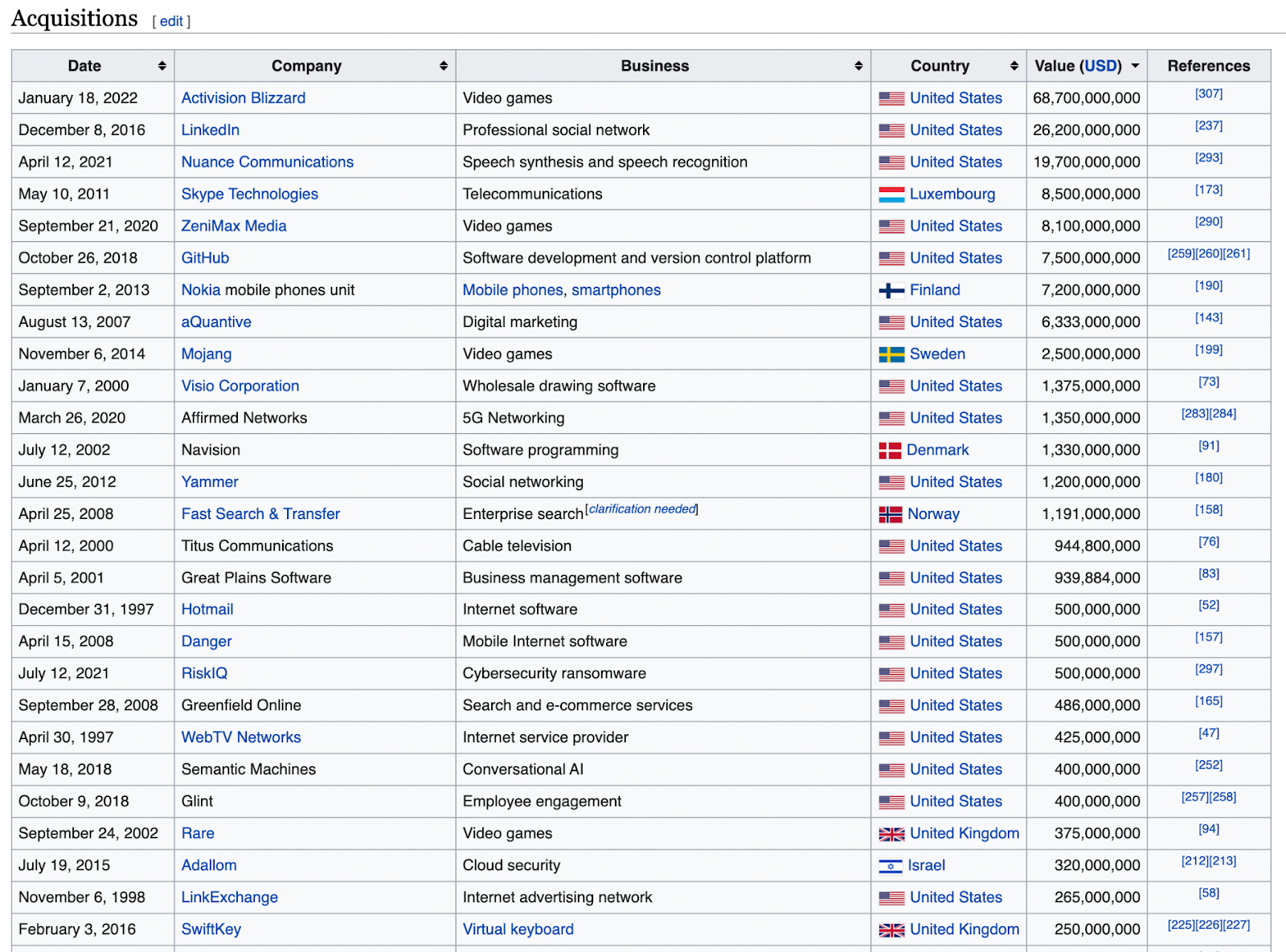

Just take a quick look at a sample of the largest acquisitions made by Apple, Microsoft, Amazon, and Alphabet, for example. (These are screenshots of the first several acquisitions by size drawn from imperfect lists collected by Wikipedia, but for purposes of casual empiricism they are well-suited to give an idea of the diversity of acquisitions at issue):

Apple:

Microsoft:

Amazon:

Alphabet (Google):

Vanishingly few of these acquisitions go to the “core functionalities” of these platforms. Alphabet’s acquisitions, for example, involve (among many other things) cybersecurity; home automation; cloud computing; wearables, smart glasses, and AR hardware; GPS navigation software; communications security; satellite technology; and social gaming. Microsoft’s acquisitions include companies specializing in video games; social networking; software versioning; drawing software; cable television; cybersecurity; employee engagement; and e-commerce. The technologies and applications involved in acquisitions by Apple and Amazon are similarly varied.

Drilling down a bit, consider the companies Alphabet acquired and put to use in the service of Google Maps:

Which, if any, of these companies would Google have purchased if it knew it would be unable to prioritize Maps in its search results? Would Google have invested more than $1 billion in these companies—and likely significantly more in internal R&D to develop Maps—if it had to speculate whether it would be required (or even be able) to prove someday in the future that prioritizing Google Maps results would enhance its core functionality?

What about Xbox? As noted, AICOA’s terms aren’t perfectly clear, so I’m not certain it would apply to Xbox (is Xbox a “website, online or mobile application, operating system, digital assistant, or online service”?). Here are Microsoft’s video-gaming-related purchases:

The vast majority of these (and all of the acquisitions for which Wikipedia has purchase-price information, totaling some $80 billion of investment) involve video games, not the development of hardware or the functionality of the Xbox platform. Would Microsoft have made these investments if it knew it would be prohibited from prioritizing its own games or exclusively using data gleaned through these games to improve its platform? No one can say for certain, but, at the margin, it is absolutely certain that these self-preferencing bills would make such acquisitions less likely.

Perhaps the most obvious—and concerning—example of the problem arises in the context of Google’s Android platform. Google famously gives Android away for free, of course, and makes its operating system significantly open for bespoke use by all comers. In exchange, Google requires that implementers of the Android OS provide some modicum of favoritism to Google’s revenue-generating products, like Search. For all its uncertainty, there is no question that AICOA’s terms would prohibit this self-preferencing. Intentionally or not, it would thus prohibit the way in which Google monetizes Android and thus hopes to recoup some of the—literally—billions of dollars it has invested in the development and maintenance of Android.

Here are Google’s Android-related acquisitions:

Would Google have bought Android in the first place (to say nothing of subsequent acquisitions and its massive ongoing investment in Android) if it had been foreclosed from adopting its preferred business model to monetize its investment? In the absence of Google bidding for these companies, would they have earned as much from other potential bidders? Would they even have come into existence at all?

Of course, AICOA wouldn’t preclude Google charging device makers for Android and thus raising the price of mobile devices. But that mechanism may not have been sufficient to support Google’s investment in Android, and it would certainly constrain its ability to compete. Even if rules like those proposed by AICOA didn’t undermine Google’s initial purchase of and investment in Android, it is manifestly unclear how forcing Google to adopt a business model that increases consumer prices and constrains its ability to compete head-to-head with Apple’s iOS ecosystem would benefit consumers. (This excellent series of posts—1, 2, 3, 4—by Dirk Auer on the European Commission’s misguided Android decision discusses in detail the significant costs of prohibiting self-preferencing on Android.)

There are innumerable further examples, as well. In all of these cases, it seems clear not only that an AICOA-like regime would diminish competition and reduce consumer welfare across important dimensions, but also that it would impoverish the startup ecosystem more broadly.

And that may be an even bigger problem. Even if you think, in the abstract, that it would be better for “Big Tech” not to own these startups, there is a real danger that putting that presumption into force would drive down acquisition prices, kill at least some tech-startup exits, and ultimately imperil the initial financing of tech startups. It should go without saying that this would be a troubling outcome. Yet there is no evidence to suggest that AICOA’s proponents have even considered whether the presumed benefits of the bill would be worth this immense cost.

The post How Tech Startups Could Be a Casualty of the War on Self-Preferencing appeared first on Truth on the Market.